06.01.26

IIUSA Webinar on Adjustment of Status Policy Update on June 4

Brought to you by Metropolitan Commercial ...

05.27.26

IIUSA Statement Regarding May 21, 2026 USCIS Policy Memorandum PM-602-0199

On May 22, 2026, U.S. Citizenship and ...

05.26.26

IIUSA is pleased to support and invite our members to participate in the upcoming 2026 Global Immigration Industry ...

05.21.26

Nearly 20 IIUSA Leadership Circle members returned to Washington, DC on May 19th for the association's quarterly ...

05.21.26

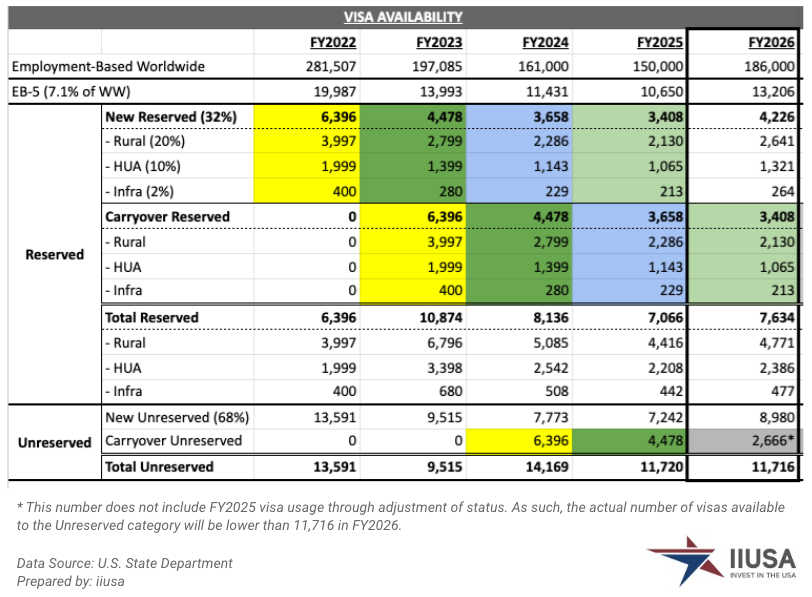

Yesterday, on May 20, the U.S. Department of State (DOS) published the much-anticipated Annual Numerical Limits ...

05.20.26

On May 19, the Bureau of Labor Statistics released the 2025 Local Area Unemployment Statistics (LAUS) annual ...

05.18.26

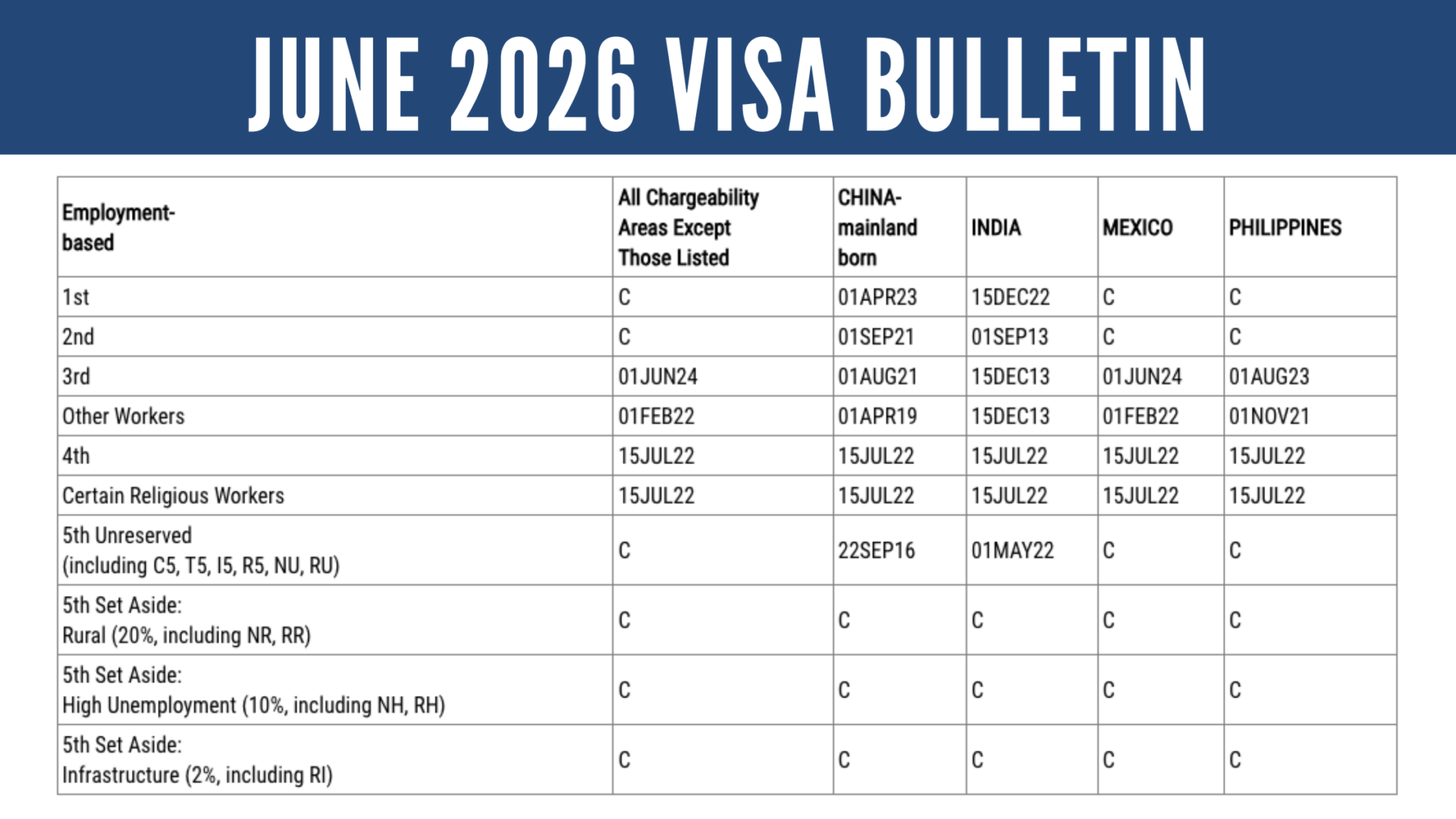

Last week, the U.S. Department of State published the June 2026 Visa Bulletin (see here), showing that all ...

05.14.26

IIUSA is pleased to announce the appointment of Ozzie F. Torres, Esq., Founder and Managing Partner of Torres Law, ...

05.14.26

Recordings Available: 2026 IIUSA EB-5 Industry Forum

From April 30 to May 1, 2026, IIUSA hosted it's 16th Annual ...

05.07.26

Washington, DC – Invest In the USA (IIUSA), the leading trade association for the EB-5 Regional Center Program, is ...

05.05.26

Spring 2026 IIUSA Regional Center Business Journal Now Available

IIUSA is proud to announce the digital ...

05.01.26

Congratulations to IIUSA's Newly Elected Board Members

IIUSA hosted its 21st Annual Membership Meeting on ...