by Scott Barnhart, Barnhart Economic Services LLC and Adam Greene, New Gen Capital

The EB-5 Reform and Integrity Act of 2022 (RIA) reinstated the Targeted Employment Area (TEA) rules instituted by USCIS in the EB-5 Immigrant Investor Program Modernization rule in November 2019, and implemented several new regional center project job-creation rules. The TEA rules require designation by USCIS and requires high unemployment TEAs to count only directly adjacent census tracts to the project tract. The new job-creation rules allow counting direct job creation for projects with construction periods less than 24 months, but also places limits on the percentage of total jobs allowed for indirect job creation.

TEAs

The TEA rules are familiar to most in the EB-5 area as they were implemented in 2019. The rules require first that USCIS adjudicate the status of TEAs (rather than individual states as was predominantly the case previously); and second that only directly adjacent tracts to the project tract can be considered for TEAs. The directly adjacent requirement severely limits the geographic area that can be considered, in some cases, to just a few city blocks. This requires TEAs to be determined by economic conditions near the project site and not in the surrounding area where the labor force might also be recruited. Even though the labor force to staff the construction at a site in, say, downtown Los Angeles could come from 10-20 miles away, the new law focuses only on a very small geographic area near the project site, rather than where the employees might come from.

Job Creation

The new job creation rules in the RIA are contained in full text in the following three subparagraphs:

INA 203(b)(5)(e)(IV) INDIRECT JOB CREATION.- (I) IN GENERAL.- The Secretary of Homeland Security shall permit aliens seeking admission under this subparagraph to satisfy only up to 90 percent of the requirement under subparagraph (A)(ii) with jobs that are estimated to be created indirectly through investment under this paragraph in accordance with this subparagraph. An employee of the new commercial enterprise or job-creating entity may be considered to hold a job that has been directly created.

INA 203(b)(5)(e)(IV)(II) CONSTRUCTION ACTIVITY LASTING LESS THAN 2 YEARS.- If the jobs estimated to be created by construction activity lasting less than 2 years, the Secretary shall permit aliens seeking admission under this subparagraph to satisfy only up to 75 percent of the requirement under subparagraph (A)(ii) with jobs that are estimated to be created indirectly through investment under this paragraph in accordance with this subparagraph.

These new rules are aimed specifically at job-creation estimated with economic models such as IMPLAN or RIMS II for regional center projects and do not apply to direct EB-5 projects at all. The following three points describe our interpretation of the new rules more succinctly (note that as of the date of this article, USCIS has not provided their guidance, policy manual or interpretation of the job creation language in the RIA):

1) (Indirect + induced) jobs in regional center projects cannot count for more than 90% of the total job count, or alternatively, the direct job count must be at least 10% of the total job count.

2) If the construction period of a project lasts less than 24 months, indirect jobs cannot count for more than 75% of the total job count, or alternatively, the direct job count in such cases must be at least 25% of the total job count.

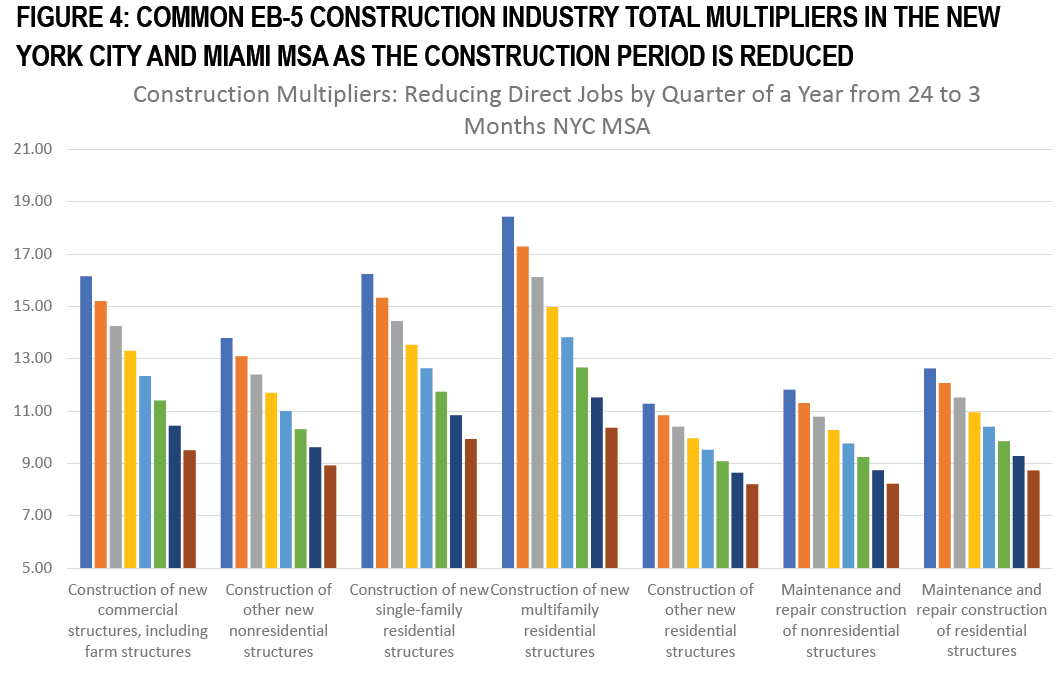

3) If the construction period of a project lasts less than 24 months, the direct job count from construction must be limited by multiplying the original direct job count by the fraction of the 24-month period that the construction lasts.

In the remainder of this article, we analyze each of the three items above in more detail. We also raise questions about the interpretation of the new rules in the final section of the article.